41 zero coupon bonds duration

What is the duration of a zero coupon bond? - Quora Originally Answered: what is the duration of a zero coupon bond? Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium. Duration: Understanding the Relationship Between Bond ... In the case of a zero-coupon bond, the bond's remaining time to its maturity date is equal to its duration. When a coupon is added to the bond, however, the bond's duration number will always be less than the maturity date. The larger the coupon, the shorter the duration number becomes.

Zero-Coupon Bond - Corporate Finance Institute As a zero-coupon bond does not pay periodic coupons, the bond trades at a discount to its face value. To understand why, consider the time value of moneyTime Value of MoneyThe time value of money is a basic financial concept that holds that money in the present is worth more than the same sum of money to be received in the future.. The time value o...

Zero coupon bonds duration

Are there bonds with zero duration? - Quora The duration is the weighted average time to cash flow, weighted by present value of the flow. For a bond with only one cash flow, such as a zero-coupon bond, duration and time to maturity are the same. But for bonds with payments prior to maturity, the duration is less than the time to maturity. 779 views View upvotes Related Answer Bill Terrell What Is Duration of a Bond? - TheStreet The easiest duration to calculate is that of a zero-coupon bond. This bond has zero yield, which means it does not pay any interest. Its duration is equal to its time to maturity. When a coupon is... Zero Coupon Bond - Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don’t mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child’s college education. With the deep discount, an investor can put up a small amount of money that can grow over many years.

Zero coupon bonds duration. The Macaulay Duration of a Zero-Coupon Bond in Excel To compensate for the lack of coupon payment, a zero-coupon bond typically trades at a discount, enabling traders and investors to profit at its maturity date, when the bond is redeemed at its face value. The Formula For Macaulay Duration Macaulay Duration = ∑ i n t i × P V i V where: t i = The time until the i th cash flow from the asset will be Zero Coupon Bond Value Calculator: Calculate Price, Yield ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months. Advantages and Risks of Zero Coupon Treasury Bonds Zero-coupon bonds are also appealing for investors who wish to pass wealth on to their heirs but are concerned about income taxes or gift taxes. If a zero-coupon bond is purchased for $1,000 and... Bond Duration Calculator - DQYDJ From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity - it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ...

PDF Duration - New York University Duration 7 For zero-coupon bonds, there is an explicit formula relating the zero price to the zero rate. We use this price-rate formula to get a formula for dollar duration. Of course, with a zero, the ability to approximate price change is not so important, because it's easy to do the exact calculation. Portfolio of zero coupon bonds and combine it with portfolio of zero coupon bonds, and combine it with the duration of a zero-spread floating rate bond to find the duration for the whole bond) Therefore, the duration of portfolio B is DB = 0.5×Dz + 0.5×Dfl = 0.5×2 + 0.5×0.5 = 1.25 For the risk-averse investor, portfolio B should be recommended since it has lower riskas measured by DA > DB. Q5. Duration of a callable zero bond - Bionic Turtle Consider a $100 face value 10-year zero-coupon bond that is callable (European-style) in one year at 80 percent of its face value. Figure 2.2 plots the bond's price, duration, and dollar duration as a function of yield. The bond price as a function of yield first steepens, and then flattens as yield increases (see Figure 2.2 Zero Coupon Bond - WallStreetMojo Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19.

Zero-Coupon Bond Definition - Investopedia A zero-coupon bond, also known as an accrual bond, is a debt security that does not pay interest but instead trades at a deep discount, rendering a profit at maturity, when the bond is redeemed for its full face value. Bond Duration Flashcards | Quizlet Duration • Duration is the term for the effective maturity of a bond • Time value of money tells us we must calculate the present value of each of the eight zero coupon bonds to construct an average • We then need to take the present value of each zero and divide it by the price of the coupon bond. Zero-coupon bond - Wikipedia A zero coupon bond always has a duration equal to its maturity, and a coupon bond always has a lower duration. Strip bonds are normally available from investment dealers maturing at terms up to 30 years. For some Canadian bonds, the maturity may be over 90 years. What is the duration of a zero coupon bond? - Quora Originally Answered: what is the duration of a zero coupon bond? Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium.

PPT - Derivatives : A Primer on Bonds PowerPoint Presentation, free download - ID:3286279

Modified Duration - Bionic Turtle Zero-coupon bonds are popular (in exams) due to their computational convenience. We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/ (1+0.04/2) under semi-annually compounded yield of 4.0%.

Duration and Convexity - Excel in CFA

Bond Convexity Calculator - DQYDJ Bond Price vs. Yield estimate for the current bond. Zero Coupon Bonds. In the duration calculator, I explained that a zero coupon bond's duration is equal to its years to maturity. However, it does have a modified (dollar) duration and convexity. Zero Coupon Bond Convexity Formula. The formula for convexity of a zero coupon bond is:

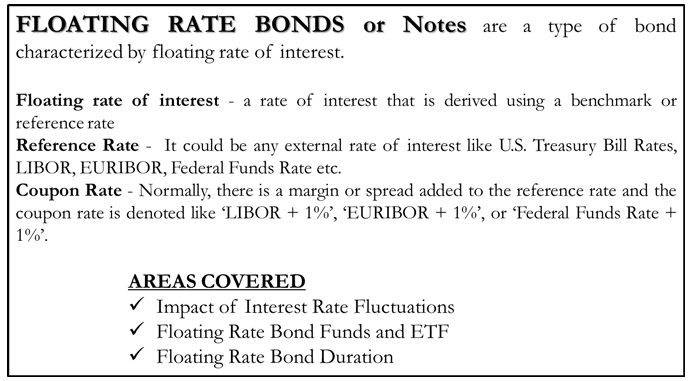

Floating Rate Bonds | Meaning, Funds, ETF, Duration, Maturity - eFM

Duration - Corporate Finance Institute It is a measure of the time required for an investor to be repaid the bond's price by the bond's total cash flows. The Macaulay duration is measured in units of time (e.g., years). The Macaulay duration for coupon-paying bonds is always lower than the bond's time to maturity. For zero-coupon bonds, the duration equals the time to maturity.

Solved: There Is A Zero Coupon Bond That Sells For $436.64... | Chegg.com

What is a Zero Coupon Bond? Who Should Invest? - Scripbox Zero coupon bonds are fixed income securities that don't pay any interest. At the time of maturity, the investor is paid the face value or par value. These bonds come with 10-15 years maturity. Hence, they trade at a deep discount. The bond pricing varies with time to maturity.

Post a Comment for "41 zero coupon bonds duration"